I recently had a very interesting conversation with a good friend. My friend and her husband are real estate investors in both South Georgia and North Florida. My friend has a theory that makes a lot of sense. She states that she has spoken to several people who are facing (and have been facing) foreclosure on their homes. Although these people have been in foreclosure, they have no idea when foreclosure will actually take place. Her belief is that this is being withheld until after November’s election so that an economic crash can be laid at the feet of Donald Trump.

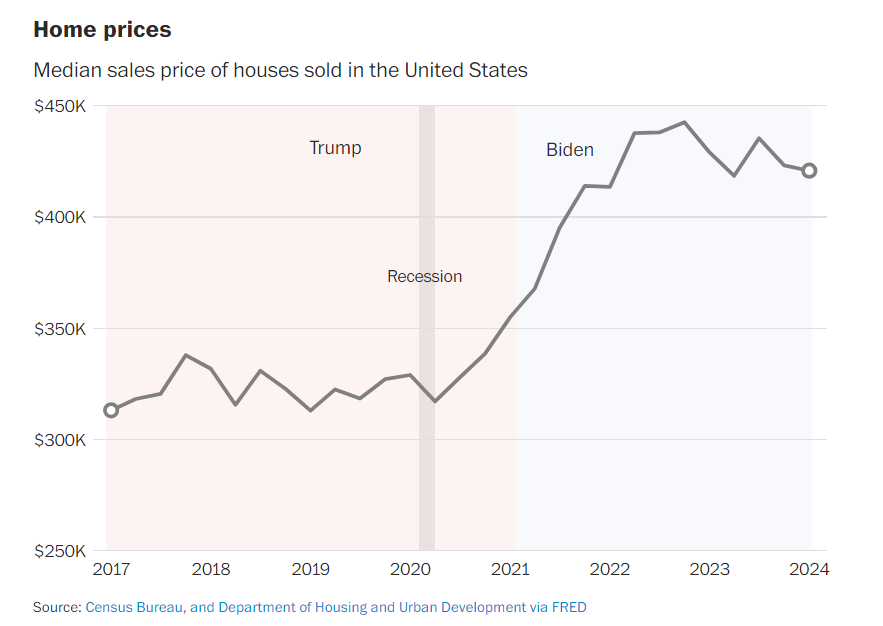

It is no secret that both home prices and interest rates have soared under Joe Biden putting home ownership out of reach for many. The American economy also appears to be artificially propped up under the Biden administration. With Kamala Harris as the current Democrat candidate, it would make sense to maintain the artificial sense of economic wellbeing, as her campaign has no viable way to escape Joe Biden’s track record. In short, an economic crash right now would spell doom for her campaign. Economic downturn through both residential and commercial real estate would be an excellent insurance policy to derail a second Trump Administration however.

In his testimony to Congress on May 15, Federal Reserve Vice Chairman for Supervision Michael Barr asserted, “The banking system remains robust and stable.”

Barr also emphasized that, “The banking sector is generally equipped to handle potential loan losses and should persist in its essential function of delivering credit to both individuals and businesses.”

A closer examination of the data indicates that a predicted surge in commercial real estate loan defaults might lead to a series of bank failures that could overwhelm the federal deposit insurance system. The concentration of commercial real estate loans and the reduced capacity of banks to absorb losses have set the stage for a situation reminiscent of the 1980s Savings and Loan Crisis.

As of the end of 2023, regulatory data shows that the banking sector held $2.1 trillion in total regulatory capital to cover losses on approximately $23.7 trillion in reported assets. Many of these bank assets have fixed interest rates and long maturities and were acquired before the Federal Reserve raised interest rates.

As of the end of 2023, I estimate that banks had $1.07 trillion in unrealized market value losses on their fixed-rate loans, leases, and securities, based on a 10-year Treasury yield of approximately 3.9 percent. Given that the current 10-year Treasury yield has risen above 4.4 percent, these market value losses are now likely closer to $1.4 trillion.

As of December 2023, the expected surge in commercial real estate loan defaults had not yet materialized in the banking system. There are signs of some banks engaging in “extend and pretend” practices with certain commercial real estate loans particularly non-owner-occupied, nonfarm, nonresidential loans from larger banks and “other acquisition, development, and construction” loans from smaller banks but there is no indication of widespread defaults.

The commercial real estate loan concentrations and performance metrics of the banking system in December 2023 closely mirror those from December 2019, before the COVID-19 pandemic led to a rise in remote work and left office buildings and shopping centers increasingly vacant.

Post-COVID, the demand for certain commercial properties has been affected by increased commuting and out-of-home dining costs, along with actual and perceived rises in urban crime due to criminal justice reforms advocated by some liberal district attorneys and elected officials.

Higher interest rates now impact both the demand for and the ability to refinance commercial real estate loans. Current interest rates are significantly higher than those in place when many existing commercial real estate loans were initially issued.

For some properties, the cash flows may not support refinancing at the new, higher interest rates, as banks generally require minimum interest coverage ratios for loan approval. In response, banks and borrowers might opt to renegotiate loan terms through troubled debt restructuring, but there is widespread expectation that, in many instances, default could become the more viable option.

Residential Real Estate faces its own set of challenges. For a recovery in the housing market to take place, several factors need to align.

Keith Gumbinger, vice president at online mortgage company HSH.com, emphasizes the importance of increasing the supply of homes for sale. “To achieve the best outcome, we’d need to see a significant rise in home inventories,” Gumbinger explains. “This increase in available homes would reduce the upward pressure on prices, potentially stabilizing them or bringing them down from their peak levels.”

Additionally, a decrease in mortgage rates would be crucial. Recent data suggests some promise in this area, with the average 30-year fixed mortgage rate holding steady at 6.78% for the week ending July 25, only slightly up from 6.77% the week before.

However, Gumbinger warns against expecting a rapid decline in mortgage rates. He suggests that if rates fall too quickly, it could lead to a surge in demand that outpaces the increase in housing inventory, causing home prices to rise again.

“It’s better if rate reductions occur gradually, improving buyer opportunities over time rather than all at once,” Gumbinger advises.

He further notes that a return to a more typical mortgage rate range of upper 4% to lower 5% would be beneficial for the housing market, potentially helping it to recover to levels seen between 2014 and 2019. However, he cautions that it may take some time before rates reach that range again.

Although more resale homes are becoming available, the inventory shortage persists and is expected to continue due to several challenges.

Many homeowners are effectively “locked in” due to their ultra-low mortgage rates and are reluctant to trade them for higher rates in a high-cost housing market. This has led to a situation where demand consistently exceeds supply, a trend likely to continue for some time.

Rick Sharga, founder and CEO of CJ Patrick Company, a market intelligence and business advisory firm, predicts, “I don’t expect to see a significant increase in the supply of existing homes for sale until mortgage rates fall to the low 5% range, which probably won’t happen in 2024.”

While new home construction has offered some relief, it has not been sufficient to significantly close the inventory gap.

According to Zillow analysis, the U.S. is currently short by 4.5 million homes, an increase from 4.3 million a year ago.

The situation is particularly acute for entry-level homes, exacerbating the cycle of heightened demand and inflated prices.

States like Florida have been affected substantially by the inflation in the real estate market. The average price of a home in 2019 was just over $250,000, while today it exceeds 400,000. Compounding the issue in some of these states are skyrocketing premiums for home owners insurance. Florida homeowners currently pay more than 4x the national average for insurance coverage.

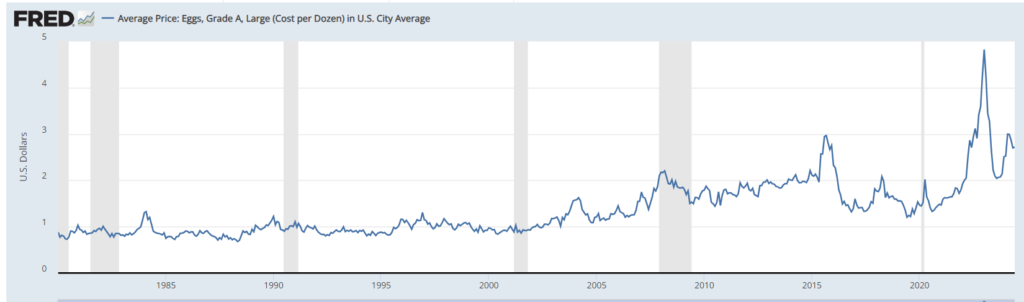

It has become common place for eggs to be a topic of discussion when discussing inflation.

Inflated egg prices in the grand scheme of things present a challenge while inflated home prices coupled with low wages and a lack of available credit are a recipe for disaster.

According to the National Association of Realtors, rates are expected to remain high throughout Q3 of 2024.

President Joe Biden pledged to reduce housing costs during his State of the Union address earlier this spring, but his plan has not yet succeeded in delivering relief.

Take the case of Anthony and Caitlin Fumo, a recently married couple with a newborn son. They had hoped their combined income would enable them to move to a larger home closer to their families. However, due to the current economic conditions, often referred to as Bidenomics, upgrading from their small rowhome in Philadelphia to a bigger property in Jersey would result in an additional $2,500 per month for their mortgage.

Anthony expressed his frustration to the Wall Street Journal, saying, “It feels like we make too much money to still feel like we’re behind.”

The latest inflation data from the Bureau of Labor Statistics suggests that the situation may not improve soon. Over the past three years, the cost of a median-priced home has more than doubled, rising by 114.5% since Biden assumed office. In contrast, consumer prices overall have increased by 19.3%, reflecting an average annual inflation rate of 5.6%.

Persistently high inflation has significantly outstripped wage increases, resulting in a 4.4% decline in real (inflation-adjusted) earnings under President Biden’s administration. Consequently, the average American’s paycheck, while about $150 larger than it was in January 2021, can purchase roughly $50 less in goods and services today.

The impact of rising interest rates on borrowing costs from mortgages to credit cards and student loans has further squeezed middle-class families. As a result, homeownership has become increasingly out of reach for many.

The stark reality is that maintaining the same house now costs a family an additional $13,300 annually compared to January 2021.

The Biden administration attempts to downplay this by citing official statistics, which suggest a 20% increase in homeownership costs over the same period. However, these figures fail to accurately reflect real-world changes in home prices and interest rates.

No amount of statistical adjustment can counteract the fact that homeownership affordability has dramatically decreased, leaving families like the Fumos and many others struggling to realize the dream of owning a home.

A common talking point for the Biden Administration is to tout the performance of Wall Street during Biden’s tenure.

It has been reported through multiple outlets that the Fed has continued to prop up Wall Street.

It is my prediction that the Deep State is planning both a residential and commercial real estate crisis to grind a 2nd Trump term to a hault. Should the real estate market experience significant casualties, expect Wall Street to follow suit. Perhaps 2008-2009 was the beta test for this strategy.

I believe that if the deep state were not planning on Trump winning, they would crash real estate markets just before Biden exits the White House in an attempt to make Kamala Harris the savior who could “fix” the problem. They do not appear to be heading this direction in the short term and appear to instead be ready to instead engage in a slow burn.

Since Trump’s historic descent down the escalator, they have engaged in every form of attacks against him including: the legal system, economic warfare during covid, media slander, and even an attempt on his life. None of those tactics have proven as effective as economic warfare. That is why I feel remarkably certain that they will revisit this tactic.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.